Commercial landlord loan delinquencies jump eightfold as vacancies and high rates bite

Rental-property loan stress is spreading through Korea’s commercial real estate market. Delinquencies have expanded eightfold in four years to about 800 billion won. Empty shops, tenant failures and high borrowing costs are eroding cash flow once seen as reliable collateral support.

Commercial landlord loan delinquencies in Korea have surged eightfold in four years, exposing a weak point in the commercial real estate cycle. Loans backed by rental buildings were long treated as stable because monthly rent supported repayment and property served as collateral. That assumption is breaking down as vacancies, small-business closures and high interest rates hit at the same time.

Rent cash flow is no longer steady

Landlords once had predictable repayment sources from restaurants, cafes and retailers. As consumer demand weakened, many tenants reduced operations or closed entirely. Empty units now leave owners covering interest payments with their own cash while they search for replacement tenants.

The pressure has deepened because borrowing costs remain high. Even buildings with some rental income can face negative cash flow after taxes, maintenance and debt service. The problem is not only lower rent but the speed at which financing costs have risen.

Delinquencies reach about 800 billion won

Unpaid rental-business loans have grown to roughly 800 billion won, eight times the level seen four years earlier. The pace of deterioration is faster than in the restaurant sector, showing that the stress from struggling tenants is moving up to landlords and banks.

For lenders, commercial property loans are becoming more sensitive to vacancy rates, local retail conditions and collateral reassessments. Loan renewals and interest resets may become tougher for buildings with weak occupancy.

What investors should watch

For landlords, the key metric is net cash flow, not headline rent. Investors need to test vacancy periods, refinancing risk and local closure rates before assuming a building is a safe income asset. Prime areas may recover faster, but weaker neighborhood retail properties are likely to remain under pressure if high rates persist.

Key points

- Rental-property loan stress is spreading through Korea’s commercial real estate market. Delinquencies have expanded eightfold in four years to about 800 billion won. Empty shops, tenant failures and high borrowing costs are eroding cash flow once seen as reliable collateral support.

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

Why are landlord loan delinquencies rising?

Vacancies, tenant closures and higher interest costs are reducing rental cash flow and making repayment harder.

How large is the delinquency problem?

Unpaid rental-business loans have increased eightfold in four years to about 800 billion won.

What should property investors monitor?

They should focus on net cash flow, vacancy duration, refinancing rates and closure trends in the surrounding retail district.

Latest stories

Mid-Rate Living Stability Loan Opens for Lower-Credit Borrowers at 5% to 15% Annual Rates

The new mid-rate living stability loan expands formal credit access for borrowers with credit scores in the bottom 50%. Rates are set in the 5% to 15% annual range, with an average target of 11% to 14%. Final pricing will depend on income, repayment ability and existing debt.

Korean Treasury Yields Rise Across the Curve as 3-Year Note Hits 3.733%

Korean government bond yields moved higher across the curve on June 29. The 3-year Treasury yield, a key market benchmark, stood at 3.733%. Rising yields mean falling bond prices and may affect bank funding, corporate borrowing and household loan rates. Investors are watching inflation, policy signals and bond supply.

Korean Treasury Yields Rise as Dollar-Won Surge Lifts 3-Year Bond to 3.733%

The dollar-won exchange rate shock spilled into Korea’s bond market. Government bond yields rose across maturities on the 29th, and the three-year yield reached 3.733%. The weaker won raised concerns over import prices, inflation pressure, and the timing of future rate cuts.

Bank loan rates to exclude legal costs from July under revised Banking Act

From July 1, banks in Korea cannot include statutory contributions and other legal costs in loan interest rates. The change reduces the room for cost pass-through in additional spreads. It is not a central bank rate cut, so the effect will differ by bank, product and borrower. A 0.10 percentage point decline saves about KRW 100,000 a year on a KRW 100 millio

Mid-Rate Living Stability Loans for Lower-Credit Borrowers Launch June 29

A new mid-rate living stability loan program starts June 29 through six savings banks. It targets borrowers with credit scores in the lower 50%. Loans carry annual rates in the 5% to 15% range and allow up to 10 million won in additional borrowing regardless of annual-income limits.

Kevin Warsh at the Fed: Greenspan Echoes, New Tests for Inflation and the Dollar

Kevin Warsh’s May 2026 arrival at the Federal Reserve invites comparison with Alan Greenspan’s 1987 debut. Both share market fluency and a focus on central-bank credibility. Warsh, however, faces post-pandemic inflation scars, fiscal pressure and supply-chain shifts. For Korea, the main channels are the won, bond yields, foreign equity flows and corporate he

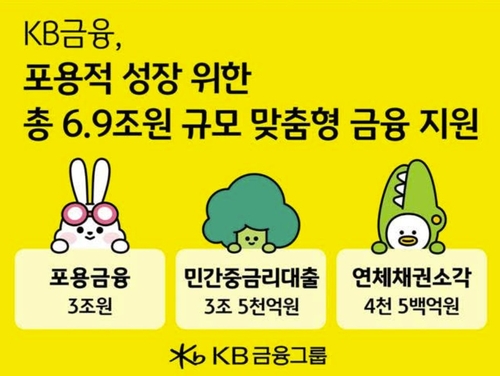

KB Financial to Expand Inclusive Finance and Mid-Rate Loans for Vulnerable Borrowers

KB Financial Group is expanding financial support for vulnerable households and small businesses this year. The program centers on 3 trillion won in inclusive finance and 3.5 trillion won in mid-rate loans. It aims to ease interest burdens and improve access to regulated finance. The move underscores the growing role of private financial groups in Korea’s in

Korean Stocks Face Inflation and Jobs Tests as Foreign Selling Signals Shift

Korean stocks have turned volatile as AI investment costs and foreign selling weigh on sentiment. Chip-sector hopes tied to Samsung Electronics and SK Hynix are cushioning the market. Inflation and employment data this week will shape rate expectations, the won-dollar exchange rate and foreign flows.