Card Loan Rates Fall for Low-Credit Borrowers, Rise for Prime Users

Card loan rates are moving in opposite directions by credit profile. Lower-credit borrowers are receiving reduced rates, while high-credit borrowers are seeing increases. The shift reflects card companies’ broader push into mid-rate loans and tighter management of funding costs and credit risk.

Card loan pricing is splitting by borrower credit profile. Rates for low-credit borrowers have declined, while rates for high-credit borrowers have risen. As card companies expand mid-rate lending, the old pattern in which the best credit scores received most of the pricing benefit is weakening.

A Shift in Card Loan Pricing

A card loan is an unsecured long-term loan offered to credit card members. It often serves as a funding route for borrowers who face limited bank loan access or need quick liquidity. The current change is not simply about an average rate moving up or down. The key point is the opposite movement across credit tiers.

Mid-rate loans are designed to serve borrowers who might otherwise be pushed into high-cost credit. Card companies are adjusting pricing while balancing inclusive finance, profitability, delinquency risk and funding costs. That has lowered the burden on lower-credit borrowers while reducing part of the rate advantage previously enjoyed by prime borrowers.

Impact on Borrowers

The data trend is clear: high-credit card loan rates have risen, and low-credit rates have fallen. Average rates alone do not capture this market change because borrowers at the top and bottom of the credit scale are experiencing different outcomes.

For low-credit borrowers, the change can ease interest costs for living expenses, medical bills or refinancing. For high-credit borrowers, it makes comparison shopping more important. Bank credit loans, internet-only bank loans and card loans should be compared by actual applied rate and repayment amount.

Outlook

Korean card companies must manage funding rates, delinquency and loan-loss costs at the same time. Expanding mid-rate loans improves access to credit, but it can also raise asset-quality risk if household repayment capacity weakens. The card loan market will increasingly be judged by rate gaps across credit tiers, mid-rate loan volumes and delinquency trends rather than headline average rates.

Key points

- Card loan rates are moving in opposite directions by credit profile. Lower-credit borrowers are receiving reduced rates, while high-credit borrowers are seeing increases. The shift reflects card companies’ broader push into mid-rate loans and tighter management of funding costs and credit risk.

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

How have card loan rates changed?

Rates have fallen for low-credit borrowers and risen for high-credit borrowers.

What is driving the change?

Card companies are expanding mid-rate loans and adjusting pricing by credit tier.

What should borrowers check?

They should compare the actual applied rate, monthly payment, total repayment and alternatives from banks or online lenders.

Latest stories

South Korea Moves Jointly to End Salt-Farm Labor Exploitation and Strengthen Sea Salt Supply Trust

South Korea is shifting salt-farm labor protection into a joint field response by the labor and oceans ministries. The effort targets wage arrears, excessive hours, suspected coercion, restricted movement, and weak safety and sanitation. For the domestic sea salt market, labor rights are becoming a supply-chain standard alongside price and quality.

Fed Market-Price Trust Test: Kevin Warsh’s Small-Fed FOMC Signal

The small-Fed debate is not simply about cutting rates sooner. It asks whether the Fed can use market prices as evidence after years of shaping those same prices. The issue runs through the two-year Treasury yield, the dollar, inflation expectations and Korea’s FX, bond and equity markets.

US June Job Growth Slows to 57,000 as Unemployment Holds at 4.2%

US employment growth slowed sharply in June, with payrolls rising by 57,000. The unemployment rate was 4.2%, pointing to a cooling but not collapsing labor market. The data is a key signal for Fed rates, the dollar, the won and Korean financial markets.

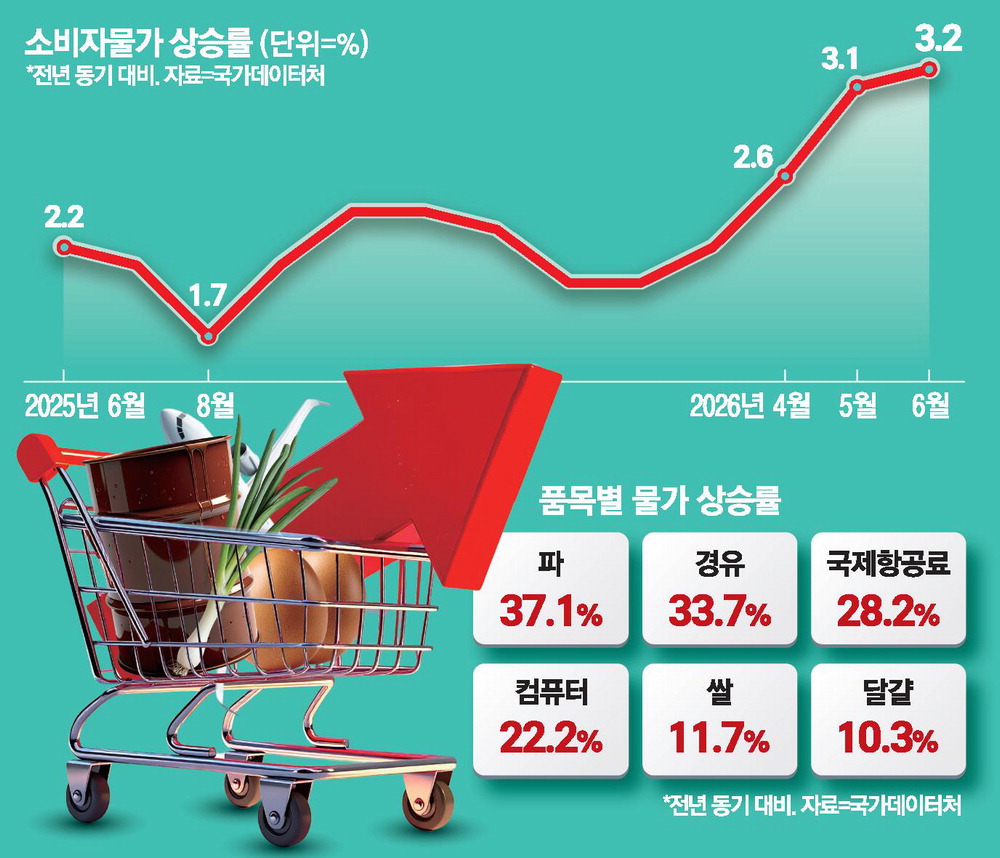

Consumer Prices Jump 3.2% as Middle East War Drives Oil Shock

Consumer prices climbed 3.2% last month, marking the largest increase in 30 months. The main driver was a sharp rise in global oil prices after the Middle East war. Petroleum prices posted their strongest rise in 47 months, while agricultural goods and daily living costs also increased. Inflation will depend heavily on oil and exchange-rate trends.

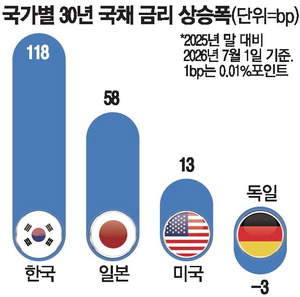

Korean government bond yields lead major-market rise as BOK hike bets return

Korean government bond yields have risen faster than U.S. and Japanese peers this year, making Korea the standout mover among major bond markets. Inflation pressure and stronger growth expectations have pushed investors to price in renewed Bank of Korea tightening risk. Higher sovereign yields can feed into bank bonds, corporate debt, mortgages and currency

KEAD Expands Mobile Job Counseling for Disabled Job Seekers at 26 Sites Nationwide

The Korea Employment Agency for Persons with Disabilities is operating mobile counseling services at 26 sites nationwide. The program reduces travel barriers for disabled job seekers and brings employment counseling closer to their communities. It aims to narrow regional service gaps and expand participation in the labor market.

Dongtan, Yongin Giheung and Guri Face Curbs as Supply and Rates Set Prices

Dongtan, Yongin Giheung and Guri have moved into a tighter regulatory zone, making a short-term slowdown likely. Stricter lending and heavier acquisition, holding and capital gains taxes will weigh on buyers. Over the medium term, home prices will depend on new supply and interest-rate direction.

U.S. Q1 GDP Revised Up to 2.1%, but Consumer Slowdown Clouds Outlook

U.S. real GDP growth for Q1 2026 was revised up to an annualized 2.1%. The figure beat the prior 1.6% estimate and confirmed resilience, but the upgrade was driven mainly by a smaller import drag. Consumer spending rose only 0.5%, while final sales to private domestic purchasers slowed to 1.7%. Korean markets must watch the dollar, Treasury yields, semicondu