Mid-Rate Livelihood Loan Launches for Lower-Credit Borrowers at 5.9% to 15.27%

The mid-rate livelihood stabilization loan launched on the 29th for borrowers in the lower 50% of credit scores. The annual interest range is 5.9% to 15.27%. It gives lower-credit households a regulated option for living expenses and urgent cash needs. Borrowers should compare repayment terms and total interest before applying.

A mid-rate livelihood stabilization loan launched on the 29th, widening funding options for borrowers whose credit scores fall in the lower 50%. The product carries annual rates of 5.9% to 15.27% and is designed to keep urgent household borrowing within the regulated financial system.

Targeting Lower-Credit Borrowers

The main target group is middle- and lower-credit borrowers who often struggle to access conventional bank loans. The loan is intended for everyday living expenses, medical bills, housing costs, education expenses and unexpected cash shortfalls. In Korea’s household credit market, this product fills the gap between low-rate bank loans and much costlier short-term or non-bank borrowing.

Rates and Repayment Burden

The headline rate starts at 5.9% and rises to 15.27% a year. On a simple one-year loan of 10 million won, interest would range from about 590,000 won to 1.527 million won before differences in repayment structure. The actual burden depends on maturity, repayment method, fees and early repayment conditions.

Borrowers should not focus only on approval odds. Monthly income, existing debt payments, card balances and any delinquency history all affect affordability. A mid-rate loan can reduce reliance on high-cost borrowing, but repeated additional debt can still raise household repayment pressure.

Market Impact

The launch could shift some demand from high-rate or informal credit channels into regulated finance. For lenders, credit assessment and risk control for lower-credit borrowers will determine whether the product remains sustainable. For consumers, the loan is a practical funding route, but only when paired with a clear repayment plan.

Key points

- The mid-rate livelihood stabilization loan launched on the 29th for borrowers in the lower 50% of credit scores. The annual interest range is 5.9% to 15.27%. It gives lower-credit households a regulated option for living expenses and urgent cash needs. Borrowers should compare repayment terms and total interest before applying.

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

Who can use the mid-rate livelihood stabilization loan?

It is aimed at middle- and lower-credit borrowers whose credit scores are in the lower 50%.

What is the interest rate range?

The annual rate ranges from 5.9% to 15.27%, depending on credit profile and screening results.

What should borrowers check before applying?

They should review monthly payments, total interest, repayment method, existing debt and early repayment conditions.

Latest stories

Mid-Rate Living Stability Loans for Lower-Credit Borrowers Launch June 29

A new mid-rate living stability loan program starts June 29 through six savings banks. It targets borrowers with credit scores in the lower 50%. Loans carry annual rates in the 5% to 15% range and allow up to 10 million won in additional borrowing regardless of annual-income limits.

Kevin Warsh at the Fed: Greenspan Echoes, New Tests for Inflation and the Dollar

Kevin Warsh’s May 2026 arrival at the Federal Reserve invites comparison with Alan Greenspan’s 1987 debut. Both share market fluency and a focus on central-bank credibility. Warsh, however, faces post-pandemic inflation scars, fiscal pressure and supply-chain shifts. For Korea, the main channels are the won, bond yields, foreign equity flows and corporate he

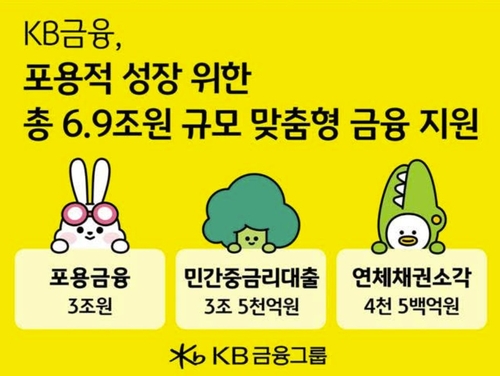

KB Financial to Expand Inclusive Finance and Mid-Rate Loans for Vulnerable Borrowers

KB Financial Group is expanding financial support for vulnerable households and small businesses this year. The program centers on 3 trillion won in inclusive finance and 3.5 trillion won in mid-rate loans. It aims to ease interest burdens and improve access to regulated finance. The move underscores the growing role of private financial groups in Korea’s in

Korean Stocks Face Inflation and Jobs Tests as Foreign Selling Signals Shift

Korean stocks have turned volatile as AI investment costs and foreign selling weigh on sentiment. Chip-sector hopes tied to Samsung Electronics and SK Hynix are cushioning the market. Inflation and employment data this week will shape rate expectations, the won-dollar exchange rate and foreign flows.

Labor Ministry Promotes Kim Cho-kyung to Standing Member of Seoul Labor Relations Commission

The Ministry of Employment and Labor has promoted Kim Cho-kyung to standing member of the Seoul Labor Relations Commission. The move centers on continuity in labor dispute mediation and adjudication for the Seoul area. Its practical significance lies in how predictably labor cases are handled for companies and workers.

New York and Shanghai Stocks Brace for U.S. June Payrolls, Rates and FX

New York and Shanghai stocks are treating U.S. June nonfarm payrolls as the week’s key macro signal. Job growth, unemployment and wage data can shift the rate path and the dollar. Korean investors are watching the won, semiconductors, autos, batteries and foreign flows into the Kospi.

Stronger Rate-Hike Signal Jolts FX and Bonds as Yields Climb

Foreign exchange and bond markets reacted sharply to a stronger rate-hike signal. Bond yields rose as investors reassessed the policy-rate path and inflation risks. A weaker won can affect import prices, foreign flows and Korean asset valuations. Markets are watching inflation data and central-bank language closely.

Rate Hike Odds and Tax-Free Dividend Hopes Lift Financial Stocks

Financial shares are gaining momentum as investors reassess earnings and dividends under a higher-rate scenario. Banks may benefit from wider lending margins, while insurers could see stronger investment income. Tax-free dividend expectations add another layer by improving after-tax cash flow. Credit costs and slower growth remain the main risks.